- Pulse by Capital Stake

- Posts

- Oil ⛽, Markets 📊, Projects 🏗️

Oil ⛽, Markets 📊, Projects 🏗️

Another Week, Another Pulse!

Just when it seemed like global tensions couldn’t intensify further, this week proved otherwise. As the world closely tracked developments in the Middle East, Pakistan quietly stepped into a more central role, hosting key regional discussions involving Iran. With conversations even touching on the Strait of Hormuz, the stakes went far beyond diplomacy, hinting at deeper strategic positioning in a rapidly shifting region.

On the economic front, there was a moment of cautious optimism. The IMF reached a staff-level agreement with Pakistan over the weekend, potentially unlocking $1.2 billion. For an economy under constant pressure, this offers some breathing room. At the same time, the IMF pushed back against Pakistan’s attempt to take greater control over state-owned enterprise, making it clear that structural reforms remain non-negotiable. The message is simple: support will come, but only alongside discipline.

Back home, the effects of global turmoil are becoming harder to ignore. Fuel prices continue to dominate the conversation, with jet fuel alone nearly tripling over time. This isn’t just about expensive flights; it feeds directly into inflation, logistics, and everyday costs. In response, the government approved a Rs. 100 billion grant to stabilize petroleum prices and shield consumers from sudden spikes. There is also growing consideration around shifting to daily fuel price adjustments, a move that could bring prices closer to global realities, but also make them far more unpredictable.

Globally, oil markets reacted sharply. Brent crude surged past $115 per barrel as conflict escalated, driven by Israeli strikes and broader regional involvement. The impact was immediate for markets like Pakistan. Foreign investors pulled out over $184 million from the domestic bond market in just the first half of March, highlighting how quickly sentiment can shift when uncertainty rises.

Despite this, there were some stabilizing developments. The government chose to keep petrol and diesel prices unchanged for another week, offering short-term relief. Iran also allowed 20 Pakistan-flagged ships to pass through the Strait of Hormuz, easing immediate concerns around supply disruptions. These moments, while small, helped prevent further pressure during an already volatile period.

The broader economic picture remains mixed. Inflation continues to rise, with the Sensitive Price Index showing an increase of over 8 percent year-on-year, largely driven by fuel costs. At the same time, monetary expansion has picked up significantly, reflecting higher government borrowing and increased liquidity in the system. More money is circulating, but it is not necessarily translating into relief for households.

Looking ahead, there are signals of potential policy shifts. The State Bank is considering an interest rate hike in response to inflationary pressures linked to the ongoing conflict. Meanwhile, the government is working on a targeted fuel subsidy system through a mobile application, aimed at supporting lower-income groups, particularly those relying on motorcycles and small vehicles. This suggests a move toward more focused and efficient relief measures rather than broad subsidies.

Energy infrastructure is also back in focus, with Pakistan expected to secure around $380 million from the World Bank to strengthen its electricity transmission system. Improving reliability in this sector could have long-term benefits, especially for businesses struggling with inconsistent supply.

Even trade patterns are beginning to reflect the changing environment. Pakistan’s trade deficit with the Middle East has narrowed slightly, though this is less about stronger performance and more about reduced activity as regional tensions weigh on economic engagement.

Amid all this, even smaller developments carried significance. Petroleum dealers postponed a planned strike, recognizing the sensitivity of the current situation and the risks of further disruption.

🎧 Tune in to this week’s Pulse:

Youtube - https://youtu.be/RZegH9Kf0kg

📅 Key Events This Week!

📌 1st April 2026

📈 CPI Inflation

⛽ Petrol Prices

📌 2nd April 2026

💱 Foreign Exchange Reserves

📌 3rd April 2026

📊 Weekly SPI

Note: These dates are tentative and subject to change. Credits: Pulse by Capital Stake

Bond Yields Skyrocket By Over 200 Basis Points in Latest PIBs Auction

The government raised Rs. 466 billion through bonds, with demand far exceeding supply, signaling strong investor confidence despite uncertainty. Yields jumped over 2%, making borrowing costlier, while the mix of tenors shows preference for longer-term debt. Next, interest rates and market conditions will determine how easily the government can fund future spending.

ADB announces support package for developing countries affected by Middle East conflict

The Asian Development Bank announced a support package for developing countries hit by the Middle East conflict, offering fast-disbursing budget aid and trade finance to secure essential imports like oil. The move aims to help countries manage immediate economic pressures while strengthening long-term resilience, with ADB ready to expand emergency support as needed. Markets and energy prices will be closely watched to guide further assistance.

Barrick delays Reko Diq project amid rising security concerns

Barrick Mining has decided to slow down development of its Reko Diq copper and gold project in Balochistan for a year, following rising security risks in the province and broader regional instability linked to the Middle East conflict. The slowdown affects timelines and budgets for what is one of Pakistan’s largest mining ventures, with over $849 million already invested. Over the next year, Barrick will continue reviewing risks and adjusting its execution strategy while keeping the project under active management.

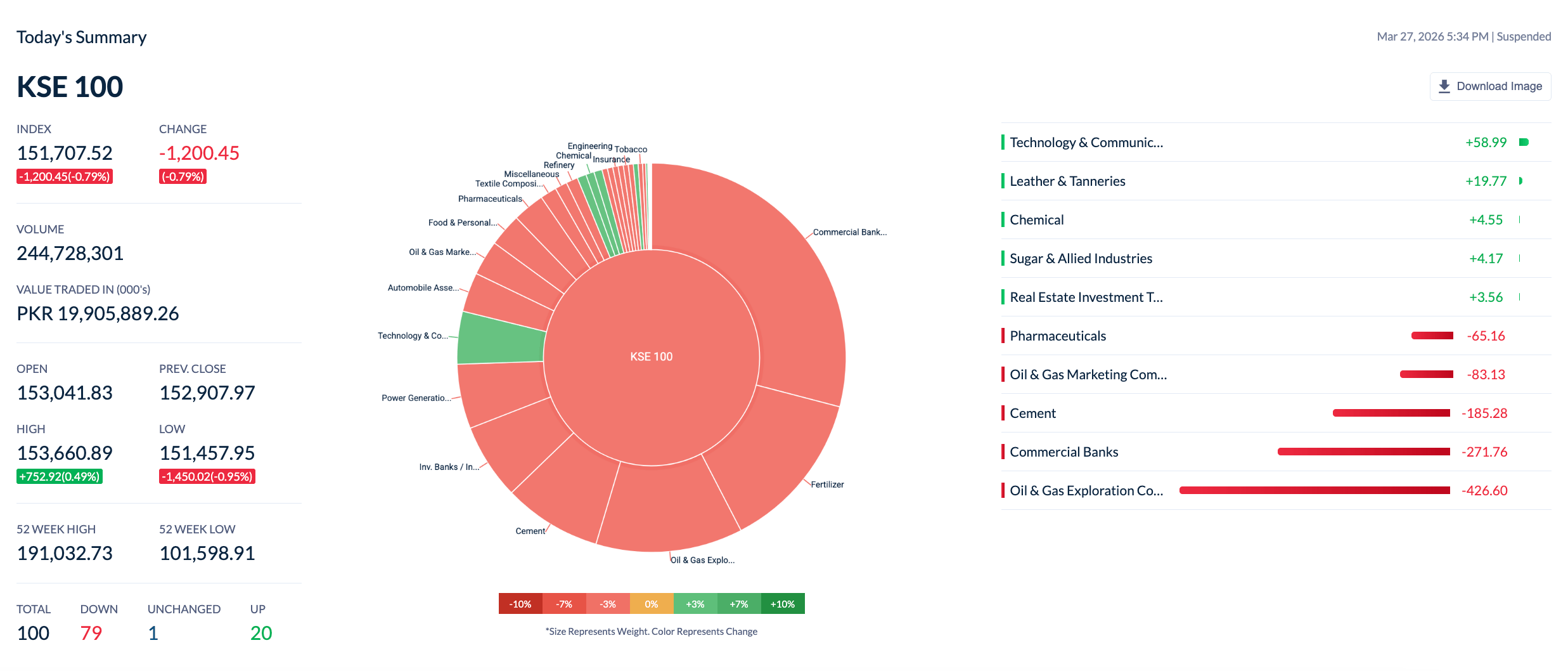

Pakistan’s stock market struggled last week, with the KSE-100 index slipping to 151,708 points, marking a 1.47% weekly decline. Persistent geopolitical tensions and swings in global oil prices kept investors cautious, even as economic developments offered some support, including progress on the IMF staff-level agreement and strong demand in the government’s high-yield debt auction, signaling healthier liquidity in the market.

You’ve been “researching” mutual funds for months. It’s time to pick one.

Scrolling through hundreds of funds? That’s the fastest way to do nothing. You don’t need every option—you need your strategy.

We’ve cut through the noise into 6 clear buckets:

High Return: Chasing the top 20 performers from last year.

Popular: Follow the money—Top 20 by AUM.

Growth: Consistency over luck—3-year performance matters.

Shariah: 100% ethical, Shariah-compliant.

Low Risk: Grow your money without losing sleep.

Start with Rs 500: No excuses—begin small, start now.

Find your fit and invest confidently: behtari.com/#collections

Get to Know More About Our Products

Behtari – Your all-in-one mutual funds investment App.

StockIntel – Your comprehensive PSX Trading and Analytics Platform.

Data Solutions – Unlock the power of data for smarter, more informed investing decisions.

Wealth Management – Smart wealth solutions for modern investors

Today’s Pulse by Capital Stake is brought to you by Hubab Irfan